Shares of Highly developed Micro Units (AMD) – Get Superior Micro Devices, Inc. Report ticked higher this week thanks to bullish news from Wall Avenue. This was a welcome progress, due to the fact AMD, together with other tech and expansion shares, experienced been trending lower this year.

Even so, even though you will find nonetheless some uncertainty concerning the superior multiples that AMD trades at, its company fundamentals glance robust. That indicates acquiring AMD although it can be still comparatively minimal may possibly be a smart go.

Let’s check out this notion additional.

Determine 1: Has AMD Stock Identified Its Way North Once more?

AMD

(Examine extra from Wall Avenue Memes: Shiba Inu Coin: Can Meme Ability Lift This Crypto Coin?)

Kumar Charges AMD as “Over weight”

On Might 17, AMD rose 8% right after being on a losing streak due to the fact the commencing of April. The key purpose for AMD’s strong functionality Tuesday was the news that Piper Sandler analyst Harsh Kumar experienced upgraded his advice on AMD shares from “neutral” to “chubby.”

The analyst attributed his new ranking to AMD’s core firms performing very well and to its extensive-expression catalysts remaining intact. In addition, Kumar reported that the acquisition of semiconductor enterprise Xilinx in February seems to be creating a solid contribution.

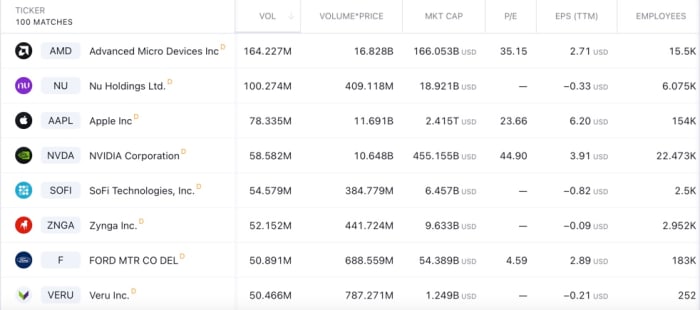

Buyers were encouraged by Kumar’s bullish ranking. On May 17, AMD was the stock with the maximum investing quantity: 164.227 million shares.

Figure 2: Most active shares on May well 17.

Buying and selling Look at

Time for a Rebound?

Stocks in basic — but particularly tech and advancement organizations — have experienced heavily amid large inflation and provide-chain disruptions. AMD’s shares have amassed losses of about 35% in 2022 on your own.

Wedbush tech analyst Dan Ives lately wrote that the present-day bear momentum in tech ought to not be considered a bubble. As a substitute, Ives said it truly is allowing for buyers to get a clearer photo of which organizations have fantastic firms. The greatest matter to do suitable now would be to analyze companies’ fundamentals and obtain those that look reliable.

Ives also believes that solid paying out will carry on in some industries, such as cybersecurity, cloud, artificial intelligence, and huge information, regardless of the current market turmoil.

As a Pc chipmaker with a presence in some of these industries, AMD has demonstrated that its fundamentals continue to be sturdy, exhibiting advancement in line with current market expectations.

So, on the lookout at the fundamentals, it is extremely possible that AMD will profit from an eventual tech current market rebound. There are other businesses whose business enterprise fundamentals are substantially even worse than their inflated stock rates recommend.

Must AMD’s Valuation Be a Concern?

The major concern about AMD is that its valuation trades at multiples that several would contemplate stretched. Its current selling price-to-earnings (P/E) ratio is 30.5 occasions. This suggests a 64% big difference from the marketplace. Rival Qualcomm (QCOM) – Get Qualcomm Incorporated Report trades at 12.8 instances, Micron (MU) – Get Micron Technology, Inc. Report trades at 8.6 occasions, and Intel (INTC) – Get Intel Company Report trades at 12.7 times.

But it really is really worth remembering that AMD is priced at high multiples due to one issue that sets it aside from its friends: its breathtaking progress reported in recent yrs.

There is in fact a possibility that AMD has potentially entrance-loaded its foreseeable future earnings. But it is also possible that this year’s selloff could have corrected ample. At the close of past year, AMD traded at a P/E ratio of close to 55 times, a great deal additional strong than the existing levels.

(Disclaimers: this is not expense guidance. The writer could be very long a person or more shares mentioned in this report. Also, the write-up may perhaps incorporate affiliate one-way links. These partnerships do not affect editorial material. Thanks for supporting Wall Road Memes)